Company

A brief explanation of components and drivers within the VASP compliance ecosystem

Publish date: 2020-11-18 12:03 | Latest update: 2023-10-10 09:00

AML/ CFT, KYC, KYT what do they mean and why are they important? A brief explanation of terms, components and drivers within the Compliance ecosystem.

Overview of AML/CFT

Regulation of financial markets and institutions are essential to cultivate trust and stability across the global ecosystem. AML (Anti Money Laundering) and CFT (Counter Financing of Terrorism) are the umbrella regulatory obligations that broadly encompasses a range of policies, procedures and controls used to detect financial crimes and their perpetrators, including KYC (Know Your Customer) and KYT (Know Your Transaction). By analyzing people, entities, wallets and transactions using AML/CFT standards a business can identify and report suspicious and illegal activity to authorities in compliance with the law. It’s estimated by the United Nations Office on Drugs and Crime (UNODC) that in one year "2–5% of global GDP, or $800 billion – $2 trillion in current US dollars''(1) is laundered globally. Entities caught facilitating transactions linked to money laundering or other illegal activities or found to be non compliant can face heavy fines, cease and desist orders, or in extreme cases even face jail time.

________

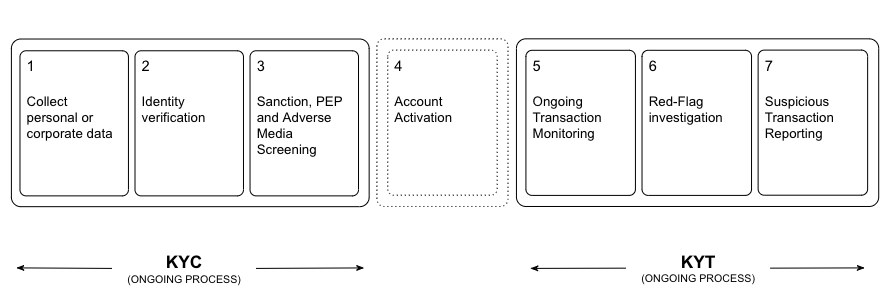

KYC - Know Your Customer

As the name suggests, (KYC) Know Your Customer is the anti-money laundering policy and procedure used to verify the identity of an individual or legal entity during the process of accepting a new customer and verify their source of funds. Regulated Financial Institutions like banks are required by law to verify several forms of identification to validate personhood before they can establish a relationship with a client. Many banks utilize third party KYC solutions to validate a new customer's information by independently reviewing their identity documents.

A KYC process may include:

■ Checking identity documents

■ Face verification

■ Validation of supporting documents such as utility bills as proof of address

■ Biometric verification

Brick and mortar businesses typically rely on physical documentation and face-to-face checks. In the case of online banks and Virtual Asset Service Providers (VASP), biometric identity verification systems are used to speed up and minimize friction during the customer onboarding experience. Some companies require a new user to hold a handwritten note with the date or other message unique to complete their virtual onboarding. More stringent KYC might include a video call to ensure the individual matches all their identity documents. Once all the details are verified the screening process takes place; using PEP, Sanctioned Lists and also scrubbing the internet for Adverse Media or other deviant behavior. Most users with an account in a prominent crypto exchange will be familiar with this onboarding process. The stringency of the verification process is a good indication of how seriously a business takes their compliance obligation.

________

KYT - Know Your Transaction

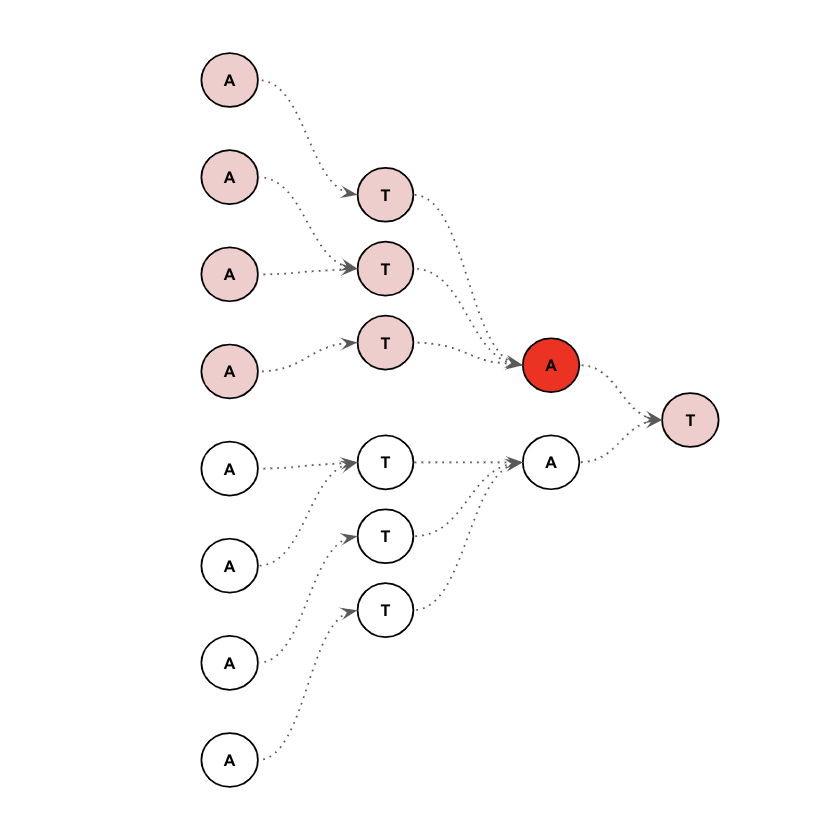

(KYT) Know Your Transaction is the process of monitoring the flow of assets to proactively identify potentially suspicious activity. For VASP companies this usually occurs by using a third party KYT Solution to continuously monitor the blockchain and scan data to identify suspicious transactions associated with illegal or high risk activities. A sophisticated KYT Solution can analyze large pools of data and use machine learning to detect patterns and Red-Flag anomalies in order to successfully determine vulnerabilities.

Industry best practice recommends using a risk-based approach to conduct Transaction Monitoring. Risk identification is done by analyzing blockchain information, cross referencing customer data sets, and analyzing the client's previous behavior in order to assign a Risk Score that typically ranges between 0 and 100. Both the wallet/ address and the individual transaction can be assigned a risk score. KYT solutions can also preemptively Whitelist or Blacklist certain wallets/ addresses to expedite the settlement time for a transaction.

Related content: Know Your Transaction - What is it and why Virtual Asset Services Providers (VASP) should care about it?

________

Standards & Recommendation

The main intergovernmental organization responsible for developing and promoting international AML/CTF standards is the Financial Action Task Force (FATF). FATF’s stated objectives are to “set standards and promote effective implementation of legal, regulatory and operational measures for combating money laundering, terrorist financing and other related threats to the integrity of the international financial system. Starting with its own members, FATF monitors countries’ progress in implementing the FATF Recommendations; reviews money laundering and terrorist financing techniques and counter-measures; and, promotes the adoption and implementation of the FATF Recommendations globally”(2).

FATF is responsible for continuously updating the now standard “Risk Based” approach to understanding how illegal activities appear transactionally, and identifying the necessary precautions needed to thwart and report them. This risk based model can be extended and applied to all areas of AML/CFT. These recommendations guide local lawmakers and help maintain a minimum set of standards for global compliance.

________

Evolving Landscape

As the virtual asset service industry grows, compliance must keep pace. The field of AML/CTF and it’s supporting technologies are posed to experience rapid growth as they become a necessary component for VASP’s to achieve regulatory compliance. In the effort to move VASP regulations closer in alignment with traditional banks, 2021 will see further implementation of the Travel Rule which mirrors the existing interbank messaging system, SWIFT. While the Travel Rule has been around since 1996 as part of the Banking Securities Act (3), in 2019 it was redefined to specify the obligations of a cryptocurrency transaction’s sender and recipient (4). Several Travel Rule solutions are currently coming to market, and will vie for market share in a battle that will determine who becomes the industry leader.

Regulating VASPs is a relatively new practice and lawmakers will continue to make sweeping industry-wide changes in the coming years; especially as governments contend to keep up with technology. Key compliance terminology must be redefined to reflect virtual assets, which will help to create continuity between banking systems. Countries like the United States that traditionally have set banking regulation precedent have taken a back seat to countries like Singapore in the race to cultivate industry friendly regulatory environments. One idea that most experts agree on, as regulations that do not hinder the industry mature, mass adoption will be within reach.

If you have any questions after reading this article, please contact our team at support@ospree.io

(1) Money-Laundering and Globalization. (n.d.). United Nations : Office on Drugs and Crime. Retrieved November 18, 2020, from https://www.unodc.org/unodc/en/money-laundering/globalization.html

(2) What we do - Financial Action Task Force (FATF). (n.d.). Financial Action Task Force. Retrieved November 18, 2020, from http://www.fatf-gafi.org/about/whatwedo/

(3) FDIC Law, Regulations, Related Acts - Miscellaneous Statutes and Regulations. (n.d.). FDIC. Retrieved November 18, 2020, from https://www.fdic.gov/regulations/laws/rules/8000-1400.html#fdic8000fra1010.410

(4) Application of FinCEN’s Regulations to Certain Business Models Involving Convertible Virtual Currencies (FIN-2019-G001). (2019, May). FinCEN. https://www.fincen.gov/sites/default/files/2019-05/FinCEN%20Guidance%20CVC%20FINAL%20508.pdf